Developing integrated financial planning solutions that embrace asset protection and tax effective structures for wealth creation, protection and distributing your wealth is crucial for protecting your business and building long-term wealth.

Here at FMG Wealth Strategists we are a team of SMExperts who in collaboration with your other advisers, develop integrated financial planning solutions that embrace asset protection principals and tax effective structures for creating, protecting and distributing your wealth.

We need to emphasize here quite strongly that your other advisers refer predominately to accountants and legal advisers whom have expertise in the area of structuring and the entities involved. Our experience here has shown best results are achieved when we blend strong financial advice and strategies together with accounting and legal specialists. This triangular approach serves the client’s best interests.

In the process of providing advice and strategies for you and your business we need to protect the wealth that you already have, protect the wealth you are going to create and to make sure that what you work hard for is yours and only yours at the end of the day.

Why build your wealth when there is a risk of someone taking it away from you?

💪 By structuring your assets for protection you also gain access to tax management strategies. We believe tax management as a by-product of asset protection and wealth creation. Effective strategies build in maximum flexibility for income distribution, which in-turn can lead to tax efficiencies.

The difference between an entity and a structure will be clarified below. An entity is the form that the operation takes on.

List of entities as follows;

- Sole Traders

- Partnerships

- Companies

- Discretionary Trusts

- Unit Trusts

- Hybrid Trusts

- Superannuation Funds

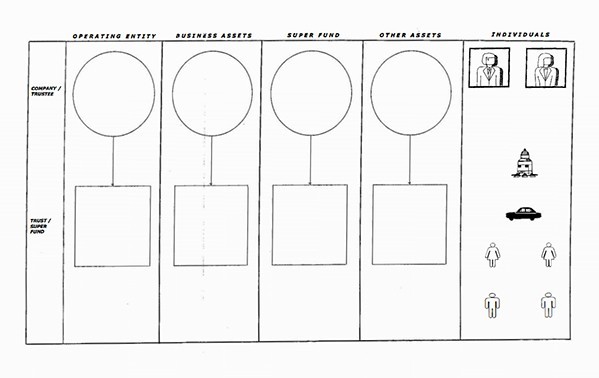

The downloadable diagram below shows the following structures in columns that refers to where a particular entity fits in.

A structure is basically an entity combination that achieves the goal of one of the following;

- Operating Structures

- Business Structures

- Superannuation Structures

- Other Asset Structure

- Individuals

For example, an operating structure may consist of a company as trustee for a discretionary trust.

Let’s begin explaining what the structures are, and how the entities fit into these structures. These structures can be used to map your current situation and suggests a plan to improve your asset protection.

Wealth Creation Pillar #1

1. Operating Structures;

The operating entity has the main risk in any group of entities. The risk of being sued is a huge concern for any business owner and multiplies every time you deal with a customer. When your family home and all other personal assets are at the mercy of the courts, your knowledge of your obligations and liabilities is priceless.

At FMG Wealth Strategists we explain the risks and the need for a complete structure. Within your structure a person is selected to take the risk. The risk taker will then remove any assets from his/her name to another trusted risk-free person.

❇️ The risk taker will only be in control of and operate the business. The risk free person will then be able to own all assets and reduce the level of overall risk to the family.

❇️ It is important to note that in family court proceeding in the case of marriage breakdown, all structures are collapsed. So the ownership of family homes, personal assets and investment assets are all available to be apportioned as if all were jointly owned.

❇️ By applying this structure setup you will broadly speaking limit the liability only to the assets of the operating entity, which should only be the cash in the bank accounts and the debtors of the business.

❇️ The next step would be to reduce any implications for the individuals who operate the entity holding minimal assets in their own names.

❇️ You can generally operate a business from any of the entities discussed above. Each has its own advantages and disadvantages and the selection of the correct entity type is imperative as all of them have different asset protection and tax consequences.

Note: Superannuation entities are not generally recommended to run an operating entity as the legislation specifically states that funds must be established for the provision of pensions or retirement benefits. Operation of a business would in most circumstances breach this.

💡 With all business owners requiring limited liability, the choice of structure is of critical importance. Your structure choice will determine access to different sources of finance, life span of your business, the ability to sell part of the business and introduce new investors or partners.

Answering the following questions will help you sort out what is required in your operating entity.

- Who is going to be the risk taker ?

- Who is going to be the safety person ?

- What assets are required to be moved from the risk taker ?

- What is the cost involved with moving the assets ?

- What tax and distribution flexibility do we require ?

- Is there a chance of capital gains resulting from the operations ?

At this point, the establishment of the risk taker is key, as all structuring decisions from this point on flow from the risk taker/safety person decision.

We will now move to the Business Asset Structure.

Wealth Creation Pillar #2

2. Business Assets Structure;

We use the term business asset structure to describe an entity that holds plant and equipment of value that the operating entity requires to conduct its day to day operations. An example is a trucking company that conducts a transport business as the operation, and has the trucks, forklifts and other infrastructure required to run it held in the Business Asset Structure.

The purpose of this is to minimize the amount of assets available to be taken during litigation in the operating entity. The safety person mentioned above is in control of the business assets and maintains separation in the eyes of the law from the operating structure, protecting the assets from creditors and litigation.

There are taxation benefits involved as well, as the operating structure is required to rent or hire the equipment from the business asset structure. This creates income in the business assets structure than can be dealt with in a more tax effective structure than the operating structure. A business asset structure can be a trust which can gain more distribution advantages than the company alone.

Questions to guide you in the Business Assets structure are;

- Is the owner /controller not the same person as the operating structure ?

- Is there a commercial basis for the hiring of the equipment?

- Are the insurances for the equipment up to date ?

- Public Liability insurance will be required as the business asset structure will be renting to the operating structure – is it sufficient ?

- Is the profit to be derived in the business assets structure able to be effectively distributed?

Your business asset structure can rent basically anything.

Beside the above example of the trucking company, consider the following;

- Doctors hiring operating theatre equipment, x-ray machines etc

- Lawyers hiring desk and computers

- Builders hiring cement mixers, utes and scaffolding

- Shops hiring shelving, cash registers and display cabinets

The possibilities are endless, so long as there is a commercially justifiable reason for hiring.

Wealth Creation Pillar #3

3. Superannuation Structures;

Superannuation generally enjoys the lowest tax rate of any structure currently in Australia.

Some of the advantages are listed below;

- Full control over where and when your funds are invested

- Family involvement – get the kids interested or combine family wealth in the most tax effective investment structure

- Ability for immediate response to opportunities

- Invest in Direct Shares, Residential and Commercial property

- More timely retirement planning options

- More estate planning options – your super benefits may be less open to challenge in a court of law if you have validly nominated where the benefits are to go

- Controllable costs on the investment and administration of the fund. The fund managers cannot take up several percentage points of your assets each year

- Effective tax management in the twilight of your life

- Your benefits may be protected from creditors.

There are 3 key limitations that superannuation funds have imposed on them.

❇️ The first is whilst you can borrow under a Limited Recourse Borrowing arrangement (LRBA) against say an investment property which allows this arrangement that the financing of this investment is separated against any other assets in the super fund it is more restrictive, costly to setup and lower loan to value ratio.

❇️ The second is that generally the fund cannot invest in related parties, which means your family and spouse’s family including all bloodline relatives, as well as companies that you are a director of or have control of cannot have funds from the family super fund.

❇️ The final key limitation is that you cannot gain a benefit from the fund assets before you retire. This happens more often than you might think. An example is if your fund owns a beach house, you cannot spend a single night in it, the other is, If your fund owns artwork, you cannot display it on the wall.

Superannuation should be the final destination for all your assets. If you are putting an amount aside purely for investment purposes, there is no reason why this amount cannot be put into your superannuation fund.

Wealth Creation Pillar #4

4. Other Assets Structures;

Your other assets structure is exactly the same as the Business Assets structure above. It is required to have the safety person in control of the structure and aims to have the same level of protection. The other Assets structure does exactly as the name suggests, that is, it holds other assets.

These are assets such as residential/commercial investment properties, shares, cash, interest bearing deposit and options, as well as more exotic assets such as artworks, vintage cars, vintage wines and other assets that you wish to protect.

Wealth Creation Pillar #5

5. Individuals;

By having established the structures described above no assets are in the risk takers name. The safety person should hold all the key individual assets, such as the family home and motor vehicle. The family home is a key asset that should in 99% of cases be held in an individual’s name. This is due to the capital gains concessions that are available.

Summary;

This overview has taken you through the key concepts of asset protection achieved through advice and strategies together with the ability to structure your different entities.

Click on the link below to download our diagram:

“5 Pillars of Structuring for Wealth Creation, Distribution and Protection”

💡 If you need more information wealth creation strategies or help in protecting your business ownership and to implement this strategy for your business and wealth protection, contact us today on 08 7111 0022. or book a chat here

REMEMBER, action is power!

We want to make the rest of your life the best of your life.

Head Office –

Suite 2, Level 1, 148 Greehill Rd,

PARKSIDE SA 5063

Ph – 08 7111 0022

Email – info@fmgws.com.au

<= SHARE THIS STORY

Disclaimer: This article is factual information only. It is not intended to imply any recommendation about any financial product(s) or to constitute tax advice. The information in the article is reliable at the time of distribution, but may not be complete or accurate in the future.