Purchase your Life and TPD Insurance Tax Effectively.

When thinking about taking out Life and TPD Insurance you may benefit by arranging the cover in a super fund rather than outside super. Find out if you can have tax-effective Life & Total & Permanent Disability (TPD) insurance cover.

What are the benefits?

By using this Life and TPD Insurance strategy, you could:

- potentially reduce the Life and TPD Insurance premium costs, and

- enable certain beneficiaries to receive the death or TPD (Total and Permanent Disability) benefit as a tax‑effective income stream.

Life and TPD Insurance Case Study 1

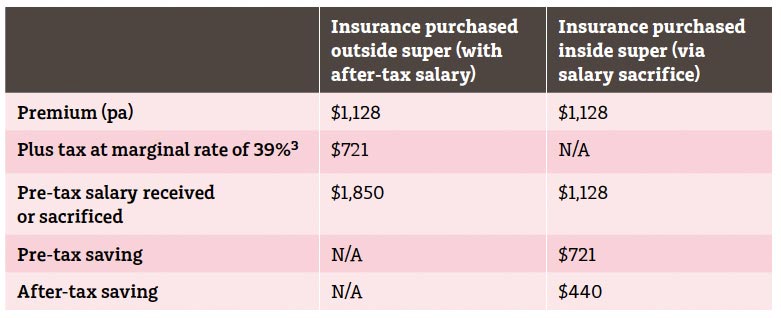

Phillip aged 50 owns a tiling business valued at $500,000. The business is run through a company from which Phillip draws a salary, and pays tax at a marginal rate of 39%.

1. Phillip wants to leave his business to his son Scott, who works in the business. As part of a strategy to treat his other son, Richard equally, Phillip’s financial adviser recommends he:

- seeks his solicitor’s advice on adjusting his Will, and

- fund the arrangement by taking out $500,000 of Life insurance, where the premium will be $1,128 in the first year.

His adviser also explains that in his case it will be more cost-effective if Phillip takes out the Life and TPD Insurance in super. This is because if he arranges for the company to sacrifice $1,128 of his salary into super, he will be able to pay the premiums with pre‑tax dollars.

2. Conversely, if he purchases the insurance outside super and pays the Life and TPD Insurance premiums himself from his after-tax salary. The pre-tax cost would be $1,850 after taking into account his marginal tax rate. (ie $1,850 less tax at 39% [$721] equals $1,128).

By insuring in super, Phillip could make a pre-tax saving of $721 on the first year’s premiums. And an after-tax saving of $440, after taking into account his marginal rate of 39%.

3. Includes a Medicare levy of 2%.

Premiums and Salary Sacrifice

4. These Life and TPD Insurance premiums are based on MLC Limited’s standard premium rates as at 28 April 2015. Formulated for non-smoking males aged 50, with $500,000 in Life cover that increases by 5% each year and includes a policy fee. In reality, they may pay different premiums based on factors such as their age, health and the amount of insurance each of them requires to protect their respective business interests.

This is for illustrative purposes only. You should refer to the relevant disclosure document before making an insurance decision.

5. Because super funds generally receive a tax deduction for death and disability premiums, no tax is deducted from the salary sacrifice super contributions. From 1 July 2012, an additional 15% tax was applied to certain concessional contributions of individuals whose income and concessional contributions exceed $300,000.

💡 The tax will only apply to those contributions in excess of the $300,000 threshold and will be assessed to the individual. Contributions on Life and TPD Insurance that are salary sacrificed must be formally agreed with your employer in an effective salary sacrifice agreement.

Tax Effective Life and TPD Insurance

Let’s now assume he continues this cover for 15 years and the amount of insurance increased by 5% pa, to ensure the benefit payable keeps pace with inflation. Over this period, the after‑tax savings could amount to $22,843 (in today’s dollars). So insuring in super could be significantly cheaper over a long time period.

Note: This case study highlights the importance of speaking to a financial adviser about the benefits of taking out insurance in a super fund. A financial adviser can also address a range of potential issues and identify other suitable protection strategies.

Tips and Traps

💰 Tax effective Life and TPD Insurance within Super

- Insurance cover purchased through a super fund is owned by the fund trustee, who is responsible for paying benefits subject to relevant legislation and the fund rules. (see ‘Restrictions on non‑death benefits’ in the Glossary.) When insuring in super, you should be clear on the powers and obligations of the relevant trustee when paying benefits.

. - Making salary sacrifice or personal deductible contributions to fund Life and TPD insurance premiums in a super fund, you should take into account the concessional contribution cap.

. - And when insuring in super, you can usually arrange to have the premiums deducted from your account balance without making additional contributions to cover the cost. This can enable you to get the cover you need without reducing your cashflow.

Level Premiums v Stepped Premiums

- While Critical Illness insurance is generally not available within super, it is possible to purchase Income Protection (or Salary Continuance) insurance in super with a choice of benefit payment periods up to age 65. Ask, to find out more about the tax implications.

. - It may be even more cost-effective over the longer term if you pay level premiums. Rather than stepped premiums that increase each year with age.

. - From 1 July 2014, own-occupation TPD and Critical Illness insurance benefits cannot be provided through super (both retail and SMSF funds). Superannuation funds can only provide insurance benefits that are consistent with the conditions of release. The continued provision of benefits to members who joined the fund before 1 July 2014 are the exception.

“MLC Protecting business owners Smart strategies guide”

Give some thought to your Life and TPD Insurance options.

Arthur Panagis

Author, Founder, Wealth Coach and Financial Strategist

B.Bus (Accountant)

Grad Dip (Financial Planning)

Professional Certificate in Self Managed Super Funds

ASX Listed Equities Accreditation

Tax (financial) Advisor

REMEMBER, action is power!

💪 We want to make the rest of your life the best of your life.

– Head Office –

Suite 2, Level 1, 148 Greehill Rd,

PARKSIDE SA 5063

Ph – 08 7111 0022

Email – info@fmgws.com.au

<= SHARE THIS STORY

Disclaimer: This article is information only. It is not intended to imply any recommendation about any financial product(s) or to constitute financial or tax advice. The information in the article is reliable at the time of distribution, but may not be complete or accurate in the future.