As a business owner, it’s your responsibility to be meeting your business expenses even if you can’t work due to illness or injury. How do you cover yourself?

Case study

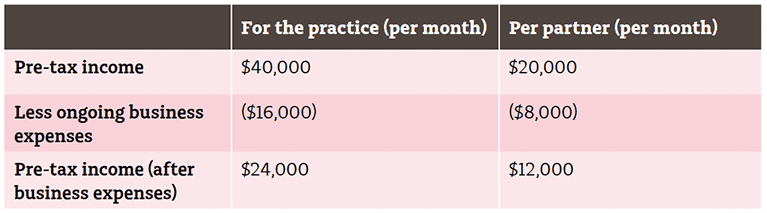

Tony and his business partner Andrew run a successful veterinary practice. They each generate a pre-tax income of $20,000 per month and are jointly responsible for meeting the total business expenses of $16,000. This leaves them $12,000 each to draw as income every month.

💰 Meeting your business expenses with the right cover

They have both used Income Protection insurance to protect 75% of their respective incomes (see Strategy 2). Tony has also taken out Business Expenses insurance for $8,000 a month, which represents his share of the practice’s business overheads.

The table below outlines what could potentially happen if either Andrew or Tony became disabled.

💰 Meeting your business expenses cont

Andrew’s Income Protection policy would provide a monthly benefit of $9,000, which represents 75% of his income, net of expenses, but before tax. However, because he doesn’t have Business Expenses insurance, he’ll have to fund the business expenses out of his own pocket – potentially from his Income Protection policy.

As a result, he’s left with $1,000 each month, which won’t be enough to cover his personal expenses, medical expenses and tax liability.

Conversely, Tony, who also insured 100% of his share of the practice’s business expenses, will not need to use any of his Income Protection benefit (or any of his personal savings) to meet his ongoing business expenses.

Note: This case study highlights the importance of speaking to a specialized financial adviser about getting insurance to cover your share of meeting your business expenses if you can’t work due to illness or injury. We are financial business protection advisers and can also address a range of potential issues and identify other suitable protection strategies.

We have some tips and traps below.

Meeting your business expenses Tips and Traps

#1. Premiums for meeting your business expenses insurance are generally tax-deductible and benefits received will generally be assessable as income, to either the business or the business owner. You should get advice from a registered tax agent relevant to your circumstances.

#2. Insurance contracts differ, so check the policy document to ensure you understand exactly what the Business Expenses insurance provides, including what are defined as eligible business expenses.

#3. You should consider insurance policies that allow you to automatically increase your cover in line with increases in the Consumer Price Index, ensuring the benefit keeps pace with the rising cost of living.

#4. It may be more cost-effective over the longer term if you pay level premiums, rather than stepped premiums that increase each year with age..

#5. Some other strategies to consider include using insurance to protect your assets, offset a reduction in business revenue, and fund an orderly transfer of business ownership..

#6. You should also make sure you have enough personal insurance to protect yourself and your family if something happens to you.

💪🏻 To find out more about any of the above and using insurance for personal protection purposes call us on 08 7111 0022 or book a chat to see how we can best help you here.

Arthur Panagis

Author, Founder, Wealth Coach and Financial Strategist

B.Bus (Accountant)

Grad Dip (Financial Planning)

Professional Certificate in Self Managed Super Funds

ASX Listed Equities Accreditation

Tax (financial) Advisor

REMEMBER, action is power!

💪 We want to make the rest of your life the best of your life.

– Head Office –

Suite 2, 148 Greenhill Rd,

PARKSIDE SA 5063

Ph – 08 7111 0022

Email – info@fmgws.com.au

👀 You can read how to further protect your wealth by protecting your income and your assets here

<= SHARE THIS STORY

Disclaimer: This article is factual information only. It is not intended to imply any recommendation about any financial product(s) or to constitute tax advice. The information in the article is reliable at the time of distribution, but may not be complete or accurate in the future.